Stacking Up Coin and Equity Offerings

In our first Coinigy Insights post, we examine how initial coin offerings (ICOs) share many similarities with traditional equity offerings by companies going public, while taking into account their inherent differences.

For many projects and startups, ICOs present a tempting way to raise money, especially when that funding could mean the difference between success and failure. In many ways, startups raising funds through ICOs and other token sales is analogous to a traditional company raising funds through venture capital and, later on, initial public offerings (IPOs).

ICOs generally serve a few different purposes. They are:

- A way for startups building blockchain-based products to raise seed funding while circumventing strict traditional venture capital regulations.

- A method of 'fair' distribution of a token in a project's early phase.

- A technique for assigning a base value through price discovery for tokens before they are actively traded on exchanges.

- A system to ensure team members and token holders are actively involved in the success of the network.

This crowdfunding mechanism can be extremely effective in situations like the ones mentioned above. Unfortunately, the conductors of many projects, both large and small, have misused or simply stolen funds that have been contributed by prospective investors and users. With the nature of digital assets in mind, these misuses show inherent difficulties that must be overcome in token sales.

While most ICOs are not selling company equity during token sales, equity offerings and token sales share many similarities. For example, tokens are often used as incentives for developers and other team members to work with timeliness and token holder interests in mind. This, paired with lockup periods and other pseudo-contractual obligations of ICO project team members, directly mirrors stock option incentive plans that companies use with executives and other employees.

An overwhelming majority of projects selling tokens are not selling cryptocurrencies, but rather cryptoassets. That is, few are exchanging raised funds in return for a coin or token whose primary function is acting as a currency for day-to-day use. In most cases, they are intended to be used on a decentralized network as a utility rather than to represent a security, a portion of equity in a company behind a project, or a peer-to-peer payment. That said, for this piece, we analogize equity representing shares of a company to tokens representing indirect 'shares' of a decentralized network.

The largest similarity between the two is the ideas behind how they are fundamentally valued. Stocks are usually valued given the present value of future expected cash flows. With this, valuations include a company's expected revenue growth, change in user base for its products, dividend schedule, and other aspects of a company. In the same way, while most tokens do not entitle a holder to any cash flows, valuing their fundamentals is quite similar. Cryptoassets can be valued on their network’s future expected growth, user base, transaction volume, and dilution from further tokens being released from a lockup or mining, among other quantifiable metrics.

Of course, ICOs and IPOs are, by nature, dissimilar in many ways as well. With traditional corporations, the company cannot be forked like an open source project can be if shareholders disagree with the direction in which it’s going. Tokens also do not offer holders the recourse that a shareholder would have; as a token holder, you are not guaranteed anything. Though these are two major points that show distinct systematic differences, they are far from the only ones.

Regardless, given the aforementioned similarities that the two share, we analyze how these offerings compare to one another.

What We’re Looking At

To analyze the comparisons between these offerings, we took a look at 30 large tech company IPOs as well as 30 of the largest ICOs, listed below.

It is important to note that while all of the companies with IPOs are tech-related, their product offerings vary widely. This also applies to the ICO projects where, though they all utilize their own token or coin and are all blockchain-based, the industry they are intended to make a substantial impact in also varies widely from project to project. Given this variation, as well as their inherent similarities to digital asset organizations, we chose to look strictly at tech companies.

The companies that held IPOs raised a combined amount of just under $60 billion, with an average of $1.99 billion and a median of $413.5 million being raised. On the ICO side, the 30 projects listed raised a total of almost $9.5 billion, with an average of $315 million and a median of $96.5 million being raised.

Further, in our sample set, the least any company raised in an IPO was $54.2 million, while the most was $25 billion. IPO numbers have been adjusted for inflation. The least raised in an ICO was $40 million, while the most was $4.1 billion.

How Do the ICOs and IPOs Compare?

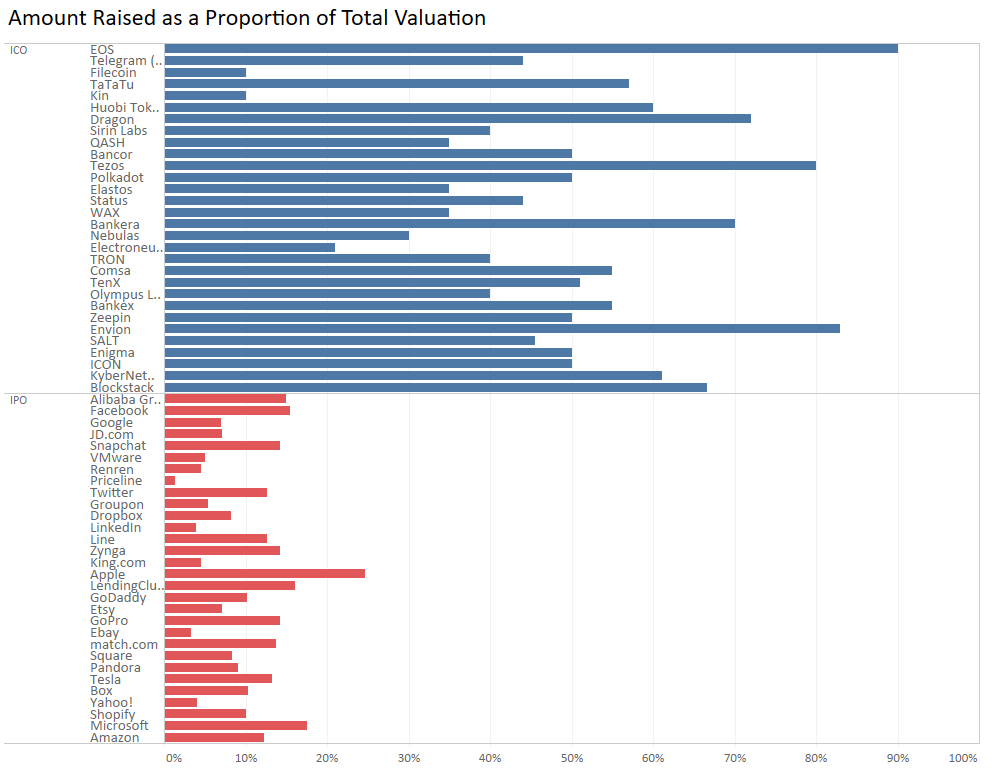

We first looked at the asset floats that resulted from these sales. Traditionally, a stock’s float is the number of shares that are available for trading (i.e. not held by insiders and other long-term holders), analogous to a token’s available supply as opposed to its total supply.

* As ordered by total valuation at conclusion of sale

From our sample, there are clear differences in trends between token and equity offerings. ICO projects typically offer far more of their asset base up for sale, as compared to traditional companies. Only three ICO projects do not have a higher float compared to all IPO companies — Filecoin, Kin, and Electroneum.

The average float for companies from their IPO is 9.55% while the median is 9.56%. Given how close these two measures are, the number of shares offered during an IPO generally follows a roughly symmetric distribution. The sample of tech company IPOs has a standard deviation of 4.50% for asset float.

On the other hand, ICOs vary far more widely. The average float for projects resulting from their ICO is 49.35%, with a median of 50.00%. The standard deviation of asset float for our sample of ICO projects is 19.09%. This shows how ICOs typically offer far more of their asset base during their sale, but also exhibit far more variation across projects.

A clear distinction comes into play with regards to venture capital and other private investment firms in ICO projects. With outside firms being shareholders of a company, there are strict rules that have to be followed with regards to disclosure, compliance, and contractual obligations between the company and private firms about when shares can be sold. With ICOs, there is little regulation or negotiation on how a crypto-fund can use or trade tokens they have bought outside of a public sale. In that way, we consider tokens sold to private firms as part of its float, as there is little restricting them from being freely traded in the open market, which cannot be said about shares held by many private investment firms.

Depending on how one looks at it, this poses a couple questions:

- Why do projects offering ICOs sell far more of the asset than companies doing an IPO offer?

- And similarly, why do companies not offer more of their stock for sale?

On a top-level basis, for traditional for-profit companies, these questions are easily answered. Both ICOs and IPOs are mechanisms for raising large sums of money, among other things. While for-profit companies generally are already making money in some form (making a profit is another story), their capital structures are also spread across both debt and equity (measured by a company’s D/E ratio).

Projects launching ICOs, and therefore already involved in the blockchain and cryptoasset space, already have an extremely hard time raising debt, given the volatility and uncertainty in digital assets. This, paired with the fact that they have no revenue at the time of the sale, is another factor that makes launching a large-scale ICO seem inviting. Through this, they can offer more of their tokens on the market in order to bring in more funds (as they have no other source).

A better metric to compare how relative these sales are is looking at assets not sold during the sale per employee. With this, we will be able to see how much of a company’s equity and a project’s token supply is held from the market, given the number of employees or team members that they have (i.e. given the size of the company/project). For the most part, projects holding ICOs are far smaller and in earlier stages of development than companies that hold IPOs, which tend to be established companies with thoroughly developed products and services.

This metric is defined by:

x = Asset Value Not Sold in Public Offering / Employee Count

We can see in the plot above that, again, IPOs have a wide range of variability with regards to equity not sold in the offering per employee. Note that the plot does not include Priceline, whose place on the plot is, literally, too far off the chart.

For this metric, ICOs had an average of $3.23 million, a median of $1.54 million, and a standard deviation of $4.33 million. Contrasting that, IPOs had an average of $12.04 million, a median of $4.83 million, and a standard deviation of $25.82 million.

Unfortunately, with the little regulation currently in the digital asset space, it can be extremely difficult to find the size of a team for a project. The data we used for employee count is based on team profiles on project websites, where available, and when that was not available, we used liberal estimates based on LinkedIn data and other sources to determine a count.

Further, we were liberal about the inclusion of tokens for the value of assets not sold in a public sale. Regardless of whether the team had allocated tokens to, say, a community development fund, they were still counted as being held by the team, as their use could (and for many projects, does) change continually.

Pulling It All Together

In traditional equity markets, firms can interact with their publicly traded stock through treasury operations. It is broadly accepted that public companies act in the best interest of their shareholders and that a firm should reward the shareholder for taking on the risk of buying its stock. The two most common mechanisms for this are dividends, both cash and stock, along with share repurchasing programs. Share repurchasing has become a point of criticism for many companies, as investors and the broader population think that firms should have better places to allocate capital. On a semi-related note, some people argue that stock buybacks are keeping much of the market afloat (example) and no one knows how long this extended repurchasing can last. Many companies within the S&P 500 are reaching critical levels of having very little stock outstanding.

So how do these public company decisions relate to cryptoasset issuance?

As more and more firms elect to issue utility tokens that will be used within their product suites, communities, and ecosystems, token treasury management will become increasingly important. But the dynamics of share repurchasing and token repurchasing are quite different.

It is obvious that publicly traded stock is a security and is held for one reason: financial gain. Some may argue that the stock is used for ownership and therefore control over the company's decision-making, but shareholders will vote for outcomes they believe will be in their best financial interest. Public companies understand this and repurchase shares to provide further financial gain to their shareholders — inherently making the stock itself attractive to other prospective buyers.

As new company structures evolve with the introduction of publicly traded tokens — which, in their most common form, are just future, discounted revenue credits — firms will begin to ask themselves if they will have token repurchasing programs. The issue here is that many crypto companies want their tokens to be non-securities and be used as micro-currencies within their app ecosystems. As William Hinman of the SEC outlined, though, if there is significant involvement by a third-party/the issuing firm, the asset becomes very security-like. That would be a big issue for many of the projects that raised funds via an ICO, as most did not sell to accredited, registered investors only. As mentioned previously, tokens are also not held exclusively for financial gain, but rather for usage and transactions.

As crypto companies elect to repurchase their tokens because they believe that the value is "too low" and that they are acting in the best interest of the token holders, it will actually hurt the usage of the token in the long run. If companies suddenly repurchase large sums of their token, the price of the service being offered by the network and the scarcity of the token will both increase, therefore decreasing the public pool and making it harder for users to obtain the token.

There is a reason that ICOs have higher public float than IPOs — it is because these assets should be used in transactional relationships and not purely for financial gain. With the current state of cryptoassets, actual use of a token beyond speculative investment is hard to come by. As the space matures and more projects hit development milestones, one would hope that we will start to see actual value being derived from the use of these tokens. That said, it is unlikely that we will see the speculative investment aspect of tokens and coins disappear entirely.

Update: Andy Bromberg of CoinList recently put out a great piece that touches on what the first hostile token takeover may look like in the future -- definitely worth the read as it relates to this Insights post.

Sources for our data collection include:

- Company S-1/F-1/Prospectus filings with the SEC for financial, employment, and IPO information

- Project websites, LinkedIn pages, and team profiles for ICO project team information

- Project websites, whitepapers, and communication with project team members for allocations of tokens (where available)

- Smith & Crown, ICO Drops, blockchain data, and other listing/news sites for determining ICO fundraising information